Bicycle insurance tailored to your needs. Select the core cover you require, then add the extras you want, and avoid paying for unnecessary protection.

Smart, flexible cover, in 3 simple steps.

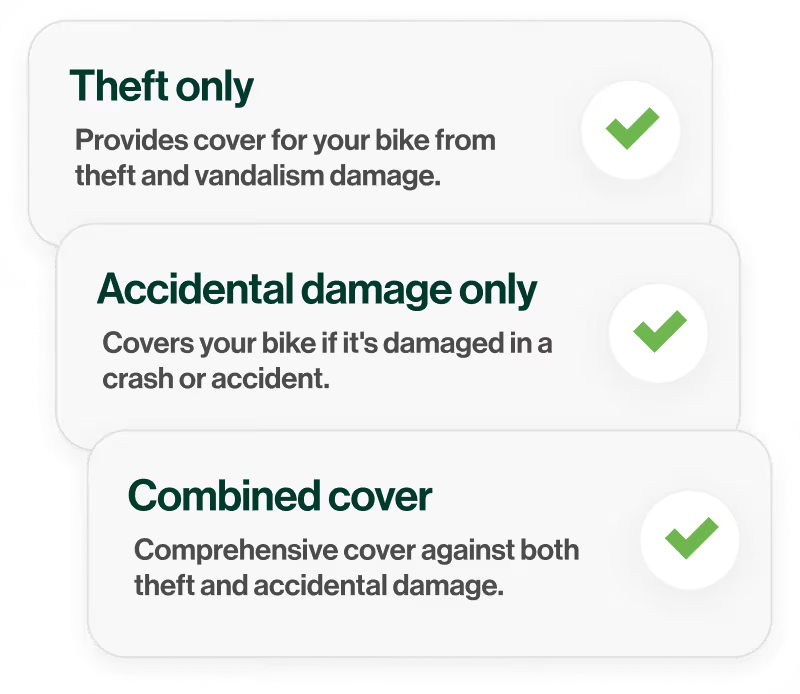

Choose your core cover

Start with the foundation. Select the core cover that’s right for you.

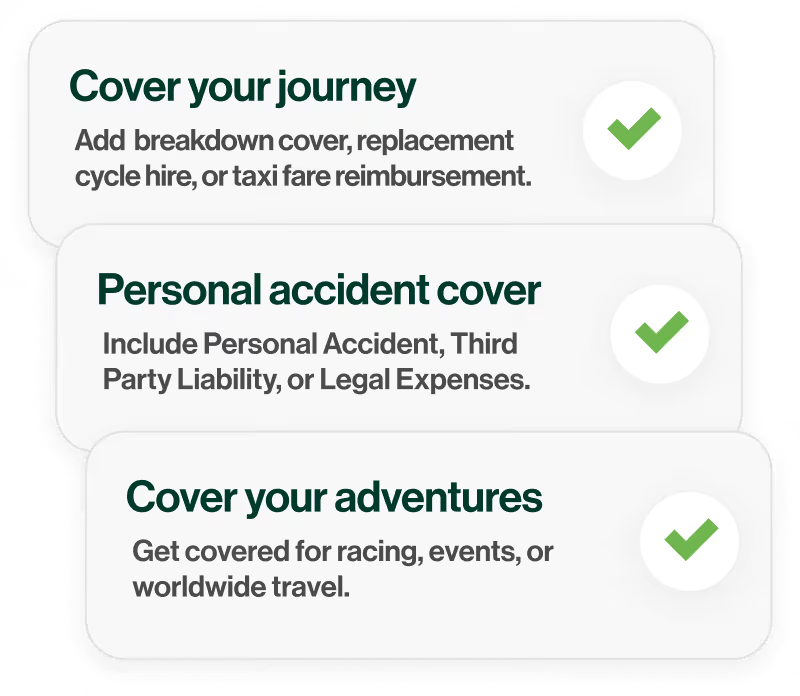

Add your extras

Customise your policy with powerful add-ons. Only pick what you need.

Ride covered

Get your instant quote and ride knowing you have the perfect cover for your journey.

More than insurance

Efficient and equitable claims

We handle claims quickly and efficiently to get you back on the road sooner.

Comprehensive breakdown assistance

Our Cycle Rescue service offers 24/7 breakdown recovery for your bicycle, e-bike, cargo bike or adapted cycle. Punctures and flat batteries included.

Over 30 years of campaigning for cyclists

For three decades we have campaigned on behalf of cyclists, championing sustainable transport and running nationwide initiatives such as Green Transport Week and In Town Without My Car.

Rated #1 for Ethics

The Good Shopping Guide has consistently recognised us as the UK's leading ethical provider in insurance, underscoring our commitment to integrity and sustainability.

Our cover options

.avif)

ETA Bicycle Insurance toolkit

Reviews for ETA bicycle & e-bike insurance

All the good things you are saying about us.

FAQs

It's simple. You start by choosing your 'Core Cover' – either Theft, Accidental Damage, or both. Then, you can add any of our optional extras, like Cycle Rescue or Third Party Liability, to create a policy that perfectly fits your needs.

If your bike is insured for under £1,500, use a Sold Secure Silver-rated lock. For bikes valued at £1,500 or more, a Gold-rated lock is required. Always lock the frame to an immovable object.

Yes, as long as they meet UK EAPC rules (max 250W motor, 15.5mph assist). Your e-bike battery is covered against theft and damage just like the rest of your bike.

Absolutely. If your main concern is theft, you can choose 'Theft Only' as your Core Cover. You can still add extras like Taxi Fare Reimbursement or our Legal Expenses cover.

Yes, our Worldwide Extension can be added to any policy and Cycle Rescue is available in the UK & EU.

Your Ride. Your Rules. Our Protection.

Call us on 0333 000 1234